B2B Purchasing and Customs Mitigation

Regarding the European VAT declaration, recently we have encountered a lot of questions from customers and friends about customs clearance and duty drawback and B2B purchasing.

Green Circle has given perfect answers and helped to handle it properly, here is one of the case studies, hopefully it can help other partners who have similar questions.

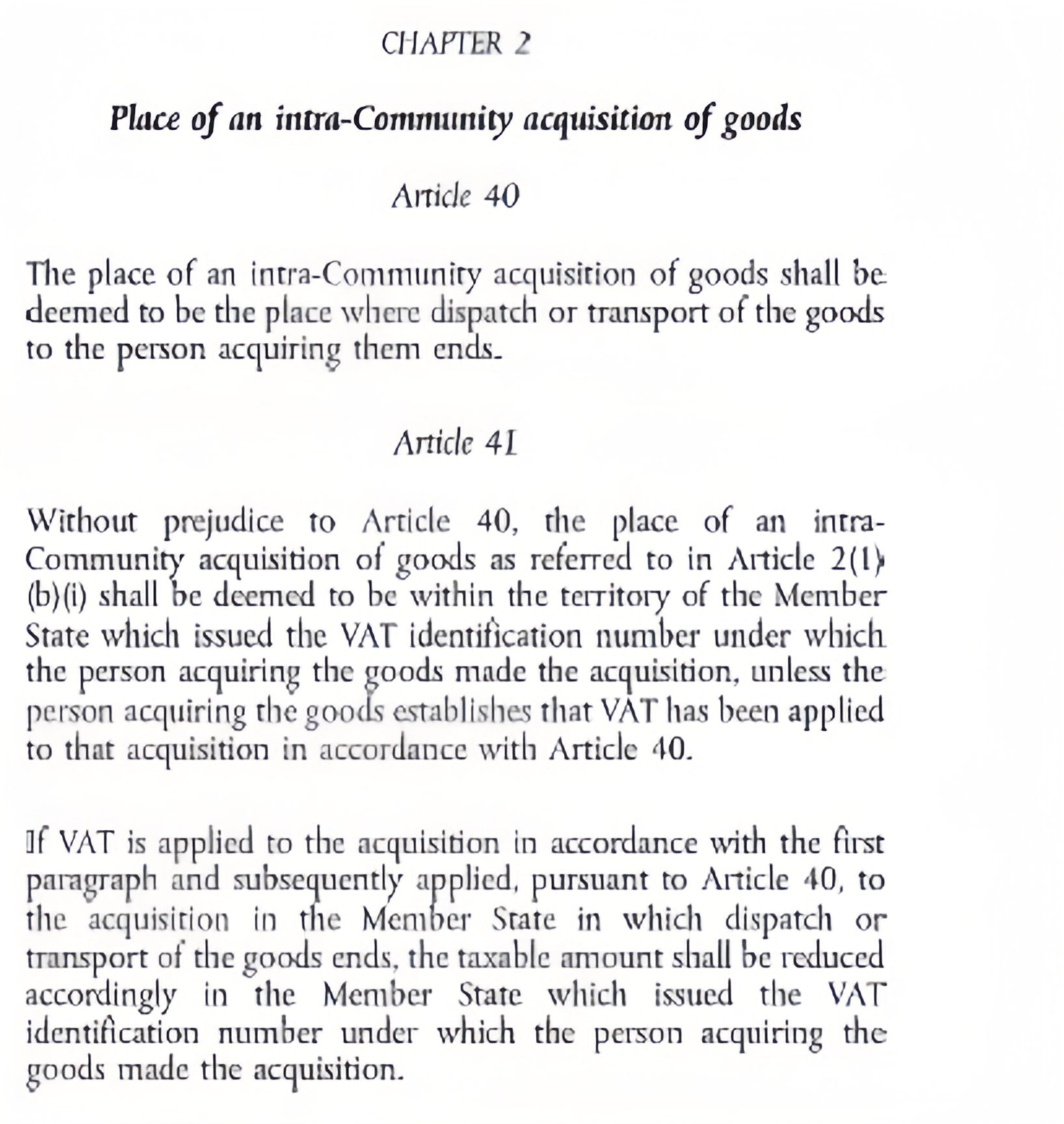

First of all, let's take a look at the German law on procurement reporting:

Below is an example of a client consultation case to explain in detail the impact of the Act on filings.

If you have any questions, we will always provide you with the most authoritative answers to your questions and solve your problems around the clock!

Client Counseling Cases

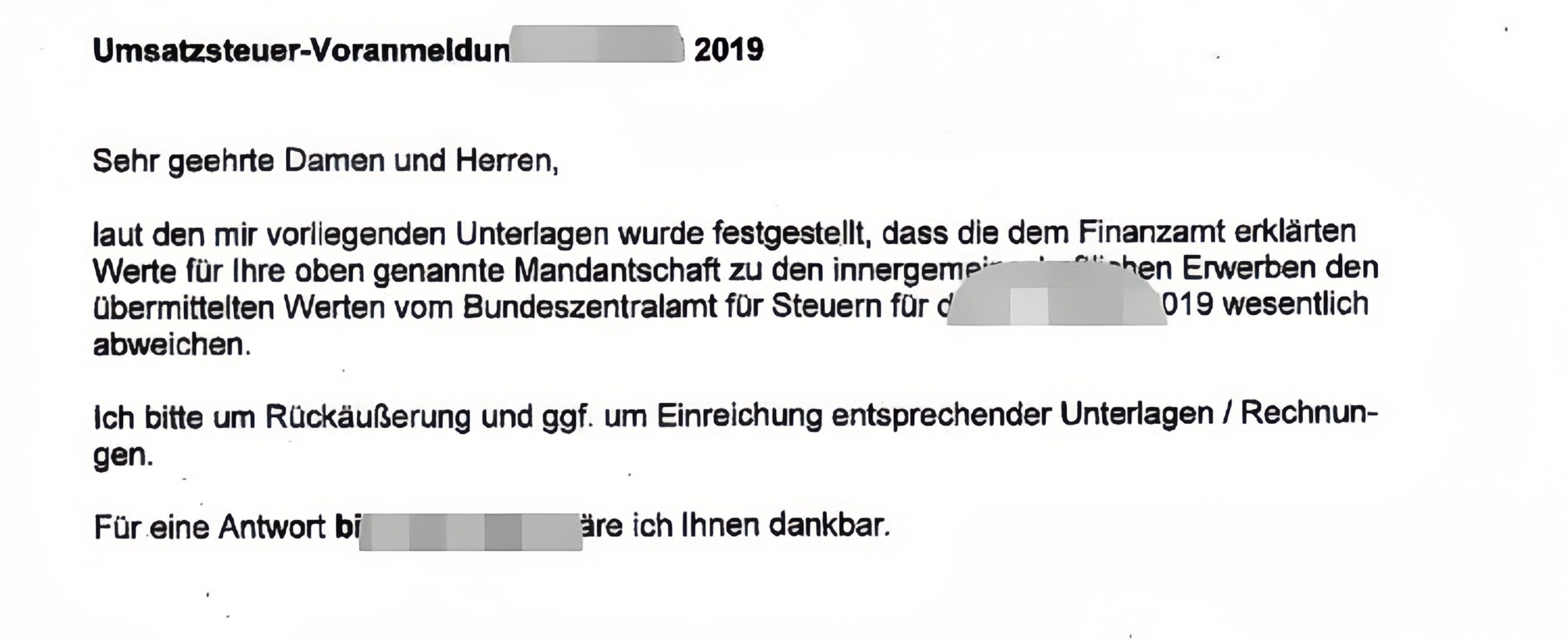

Q: Ms. Green Circle, I received a letter from the German tax office, can you explain it to me?

A: Hello, this is a letter from the German tax office asking you to provide B2B purchase orders from previous seasons for reporting.

Q: Do I need to report B2B purchases and what are B2B purchases?

A: B2B procurement is what I say in the day-to-day ECSales procurement orders, EC SALES is that if the EU registered VAT tax number and to other non-domestic but have the EU tax code of the business enterprise merchant sales orders, this part of the sales should be zero tax rate, that is, the so-called reverse charge system.

B2B purchasing means that you purchase from VAT-registered merchants in other European countries.

It also includes customs clearance and tax deferral.

Q: Why is it related to customs clearance and duty drawback?

A: For example, your goods are cleared from an EU country and sent directly to Germany. Customs clearance bank in the customs clearance country applied for a customs clearance holdover, that is, you imported in the EU region did not pay import VAT, at the same time in Germany when the sale of import VAT can not be carried out refund operation, then this situation is equivalent to your German tax code registered company to the customs clearance country to carry out a B2B zero-tax procurement. This is equivalent to a B2B sale in the country of customs clearance and a B2B purchase in Germany, which also needs to be reported in the VAT return.

Q: Do I have to pay additional taxes?

A: Since your supplier and yourself have registered tax IDs in different EU countries, this part of the order is tax-free according to the previous EC SALES sales rules.

Q: How will the IRS know I have B2B purchases?

A: Your supplier will report B2B sales when filing the sales VAT return, and then the IRS will be able to know that you have made the purchases.

Q: How should I report this?

A: It needs to be filed by your tax agent at the time of monthly/quarterly filing.

Green Circle Tax Tips

What is VAT Tax Buffer Clearance

VAT tax mitigation, also known as fiscal clearance;

a. Goods enter the EU country of declaration and pass through the tax buffer to the final country of distribution.

b. Sellers only need to pay customs duty in the country of filing and do not need to pay import VAT.

c. Sellers can choose to import from the Netherlands or Belgium, and when the destination country of the goods is another EU member country, they can choose the VAT holdover method, i.e. sellers do not need to pay import VAT when importing goods.

d. VAT tax mitigation is legal and compliant, it provides room for businesses to turn around their capital and is therefore the preferred option for many sellers.

If you have more questions about B2B procurement reporting, please contact our dedicated account manager.