Austria is one of the most prosperous countries in the European Union, and in recent years, online sales have grown significantly faster than physical store sales. As the new star of Amazon Europe, Austria's strong purchasing power has been favored by more and more Chinese sellers. Today, the green circle editorial first bring everyone together to understand and learn the basic knowledge of Austrian VAT, help sellers to explore the new land.

Distance selling

The current threshold in Austria is 35,000 Euro (since 1 January 2011).

Remote Sales Threshold

Austria's remote sales threshold from January 1, 2011 is 35,000EUR.

Current legal basis

In general, if goods are dispatched or transported from an EU-Member State to Austria by a foreign supplier or on behalf of a foreign supplier to the below-mentioned customers, the supplies of goods are generally taxable where the goods are located at the time when dispatch or transport of the goods to the EU-Member State is taking place. In general, if goods are dispatched or transported from an EU-Member State to Austria by a foreign supplier or on behalf of a foreign supplier to the below- mentioned customers, the supplies of goods are generally taxable where the goods are located at the time when dispatch or transport of the goods to the The customer begins.

For distance selling however, there are special rules. Article 3 (3) - (7) Austrian VATAct 1994 stipulates that the place of supply of goods dispatched or transported by or on behalf of the supplier from an EU-Member State to another is the place where the goods are located at the time when the goods are sold. The Austrian VATAct 1994 stipulates that the place of supply of goods dispatched or transported by or on behalf of the supplier from an EU-Member State to another is the place where the goods are located at the time when Distance selling regime applies to certain types of recipients (especially private individuals) as Amazon final consumers. Distance selling regime applies to certain types of recipients (especially private individuals) as Amazon final consumers.

Current legal basis

Generally speaking, if the goods are sold to Austrian consumers by a seller from outside the EU (non-EU, e.g. our Chinese company) who has warehouses in an EU-member state and ships the goods from a warehouse in an EU-member state, they should generally be taxed in the place where the goods are situated within the EU (the country of shipment).

However, Section 3(3)-(7) Austrian VATACT1994's remote sales regime, which provides for the sale and delivery of goods to Austrian end-consumers by sellers outside the EU from warehouses located in EU-member states (non-Austrian EU countries), applies specifically to sellers trading as Amazon B2C.

Example.

German entrepreneurs or Chinese entrepreneurs with warehouses in Germany transfer goods from Germany to individual buyers in Austria. If the total sales volume in a year exceeds the threshold of 35,000 euros, then the sales volume from the time it exceeds 35,000 euros is subject to VAT in Austria. German or Chinese entrepreneurs must register a VAT number for the purpose of registering and paying VAT in Austria, and invoices issued to these Austrian individuals must show the Austrian VAT rate!

Note: Entrepreneurs who have not established a business in Austria or do not have a permanent location are not eligible to use the Small Business Program under Article 6, paragraph 1, item 27 of the Austrian Value Added Tax Act 1994, (i.e., the Austrian Small Business Program is not suitable for business sellers who do not have an Austrian warehouse).

How to calculate the threshold

The delivery threshold must be calculated separately for each member country. When calculating the delivery threshold, only sales from distance selling regime should be taken into account. When calculating the delivery threshold, only sales from distance selling regime should be taken into account.

Intra-community deliveries, charges for the delivery of new vehicles, charges for the delivery of excise goods and sales subject to differential taxation are excluded. Intra-community deliveries, charges for the delivery of new vehicles, charges for the delivery of excise goods and sales subject to differential

Entrepreneurs from other EU countries who deliver to private individuals in Austria must invoice with Austrian sales tax from the following time.

- 1. If the delivery threshold is exceeded in the previous year: billing with Austrian VAT from the 1st turnover of the current year.

- 2. If the delivery threshold is exceeded in the current year: Invoicing with Austrian VAT from the sales with which the delivery threshold was exceeded. was exceeded.

How to Calculate Austrian Remote Sales Thresholds

Sales to Austria from each country are calculated separately, and then sales to Austria from non-Austrian countries are summed up, and this sum is used to calculate remote sales to see if they exceed the Austrian threshold (35,000 euros).

Corporate sellers with inventories from other EU countries are required to register for an Austrian tax code and pay VAT in Austria under one of the following conditions:

- 1. If the previous year exceeded the remote threshold of €35,000: Austrian VAT is due in Austria from the first turnover of the year.

- 2. If the remote sales threshold is exceeded in the year, Austrian VAT is calculated from the sales above the delivery threshold.

New EU regulation 2021

Please note that the threshold will be generally abolished beginning with 2021. That means from 2021 on distance sales will have to be taxed in each EU member state where the dispatch or transport ends. That means from 2021 on distance sales will have to be taxed in each EU member state where the dispatch or transport ends.

New EU Regulation 2021

Please note that the new EU legislation removes the sales threshold from 2021. This means that from 2021 onwards, remote sales will be taxed in the EU member states according to the country of shipment or the country of destination, and there will be no sales thresholds as described above.

Application for a tax account number or a VAT number

Following documents are required for application.

- Verf 19: Questionnaire for the assessment procedure

In addition: indication of sales channels (e.g. homepage, catalogue etc.)

Note:distance sellers are usually not allocated a VAT number since they only need a tax account number to account for the VAT due. However, if they need a VAT number, they have to fill in form 'Verf 19' giving sufficient reasons for their request. However, if they need a VAT number, they have to fill in form 'Verf 19' giving sufficient reasons for their request.

- Verf 26: specimen signature sheet

- Valid VAT number or certificate of registration as taxable person (entrepreneur) issued by the Tax Office of the country the entrepreneur has established his business in (original)

- Copy of the company statutes

- Copy of the manager's passport / ID

- Copy of the certificate of registration

What do I need to apply for an Austrian VAT number?

The following documents are required to apply:

-(1) Assessment Questionnaire (Verf19)

Note: Remote sellers are not normally issued with a VAT number by the Inland Revenue, however, if they require a VAT number, they must complete the "Verf 19" form to fully explain their requirements.

-(2) Application for signature (Verf 26)

-(3) Valid VAT number or certificate of registration issued by the tax authorities of the country/region in which the company carries out its business (taxable person)

-(4) Scanned copy of Articles of Incorporation (for backup)

-(5) Photocopy of corporate passport/identity card

-(6) Photocopy of the company's business license

Tax Representative

The appointment of a Fiscal Representative is only mandatory if the supplier has no permanent address, seat or fixed establishment in an EUMember State and if there is no appropriate mutual agreement procedure. The appointment of a Fiscal Representative is only mandatory if the supplier has no permanent address, seat or fixed establishment in an EUMember State and if there is no appropriate mutual agreement procedure.

Tax Representative

The appointment of a financial representative is only mandatory if the seller does not have a fixed address, seat or establishment in an EU member state and there is no legal agreement between the parties. The financial representative must also be authorized as a recipient of correspondence from the Inland Revenue.

Disclosure/ Report of Incorrect or Incomplete Tax Declaration

If you have exceeded the Austrian distance selling threshold of EUR 35,000 Euro in previous years, but have not declared these supplies in Austria, you If you have exceeded the Austrian distance selling threshold of EUR 35,000 in previous years, but have not declared these supplies in Austria, you have to subsequently correct this and declare them in Austria. You can either report an incorrect or incomplete tax declaration to the tax authorities or fully disclose these supplies.

Disclosure/reporting of incorrect or incomplete tax returns

If you have exceeded the EUR 35,000 threshold for Austrian distance sales in previous years but have not yet reported these sales in Austria, you must subsequently correct this status and report them in Austria. You can report incorrect or incomplete tax returns to the tax authorities or fully disclose the status of these sales.

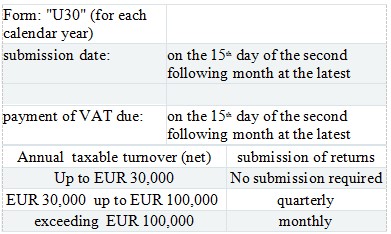

Submission of VAT Returns

In Austria there are VAT advance preliminary returns and VAT annual final returns.

- a. Preliminary VAT return

- b. Annual VAT return

Submission of VAT returns

In Austria, the VAT return requires the submission of an initial advance payment report and an annual VAT return.

-Preliminary Prepayment Report (i.e., monthly or quarterly)

(1) As of the filing date is the 15th day of the second month of the following month, (e.g., sales reports for May must be filed by July 15)

(2) VAT payable: no later than the 15th day of the second month of the following month.

▫ Annual Return of Taxable Turnover (Net)

1. If the pre-tax sales for a year are less than €35,000, no monthly or quarterly report is required.

2. If the pre-tax sales for a year is more than 35,000 Euros and less than 100,000 Euros, then quarterly reporting is allowed.

3. Monthly reports are required if pre-tax sales in a year exceed €100,000.

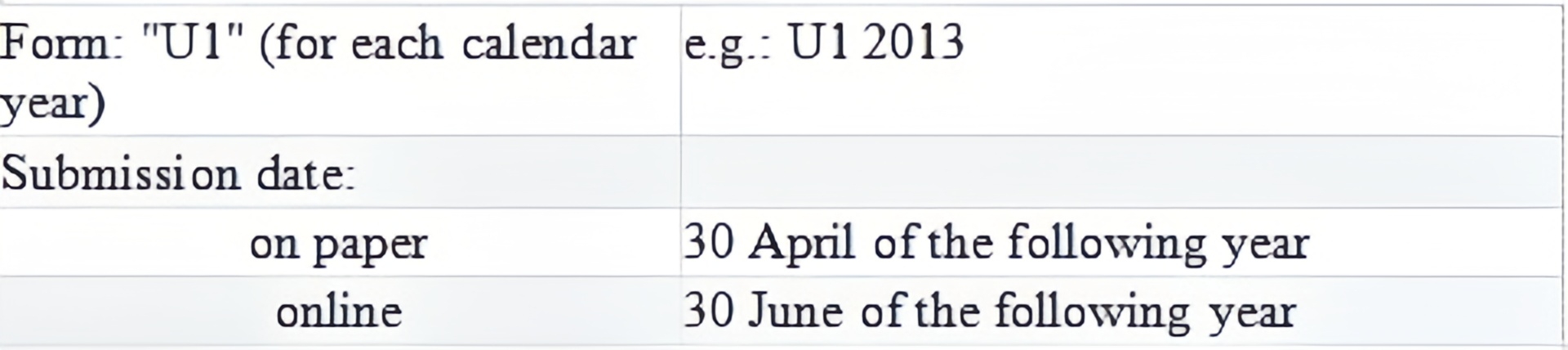

-Annual VAT Return (also known as Annual Report)

Submissions can be made online or by paper mail. The deadline for online submissions is June 30 of the following year, and the deadline for paper mail submissions is April 30 of the following year.