Europe VAT# Switzerland VAT

As required by Swiss VAT law, as of January 1, 2019, sellers are required to register for Swiss VAT as long as they have global sales of CHF 100,000 and have generated sales on the Swiss market. In this case, the cross-border seller must complete the Swiss VAT registration obligation within 30 days and file a VAT tax return in accordance with the law.

01

Switzerland VAT Registration

Register

Swiss VAT regulations also make it clear that both domestic and foreign companies are obliged to register for VAT, provided that the following conditions are met:

◆ Importing goods in Switzerland;

◆ Buying and selling goods in Switzerland;

◆ Online business for Swiss consumers;

◆ Storage of goods in local Swiss warehouses and resale to Swiss buyers;

◆ Provision of services in Switzerland under reverse VAT rules

Switzerland has adopted most of the EU VAT place of supply rules, including the use of reverse charging, which means that few service-related situations have required VAT registration since the EU's 2010 VAT package.

As of January 1, 2019, and for a period of 12 months thereafter, sellers must register in the VAT register and pay VAT in Switzerland whenever they send low-value goods from abroad to Switzerland that generate sales of CHF 100,000 or more.

02

Swiss VAT tax rate

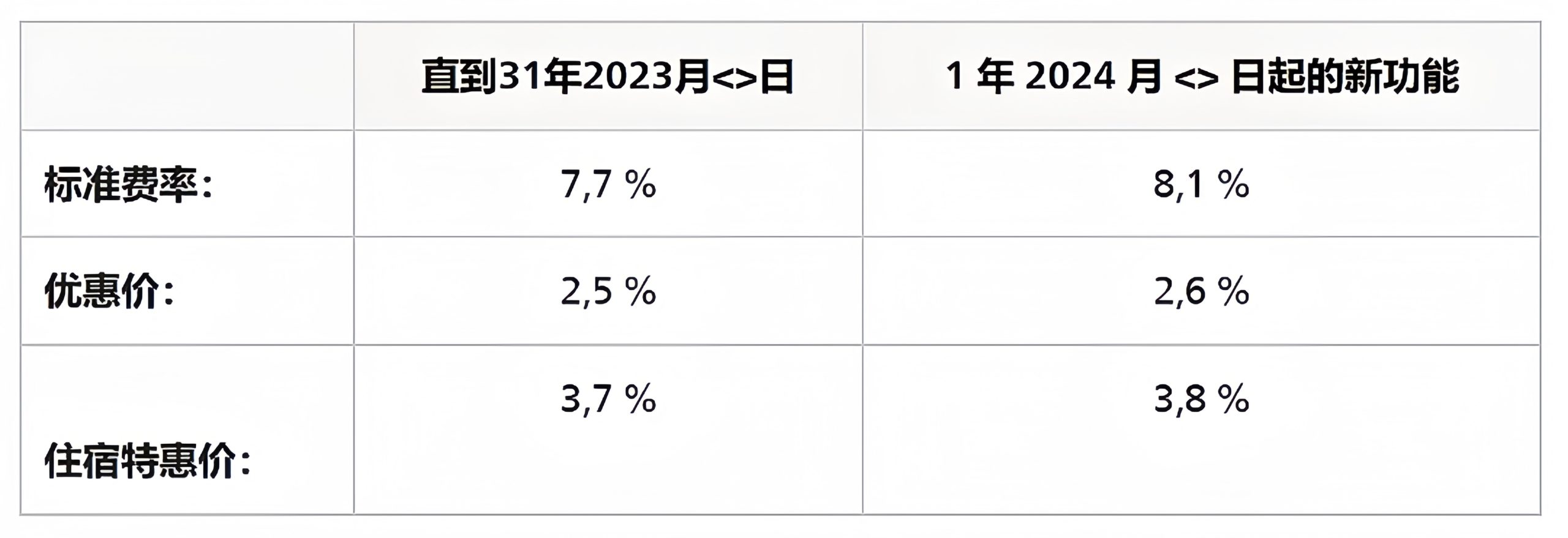

Standard rate of 7.7%: applies to the vast majority of goods;

Concessionary rate of 2.5%: Applicable to food, pharmaceuticals, newspapers and publications;

Special tax rate 3.7%: applies to lodging with breakfast.

According to the latest draft resolution of the Swiss Tax Administration, the VAT rate is planned to increase on January 1, 2024, with the standard rate increasing from 7.7% to 8.1% and the preferential rate of 2.5% to 2.6%.

03

Swiss VAT Filing Cycle

Swiss VAT returns are generally filed quarterly, four times a year; if a taxpayer applies for tax under the net rate method, a VAT return must be filed every six months.

The deadline for filing a VAT return is normally 60 days after the end of the VAT settlement period along with full payment.

04

Swiss VAT refund

All earnings in Switzerland are subject to VAT. Companies that pay VAT in Switzerland have the opportunity to receive a refund from the Swiss government. Some foreign companies are entitled to a VAT refund once a year, not everyone. A refund can be established if the owner completes an application form and submits it to the Swiss Federal Revenue by June 30 of the following year. The original invoice and proof of VAT registration in Switzerland must be provided. If the evidence is accepted, the owner will receive the refund within 6 to 9 months.