With the opening of the Amazon Middle East station, more and more sellers began the Middle East road to gold. We also encountered a lot of Middle East station UAE sellers have started a period of time FBA sales, registration VAT tax number only to find that they missed the required registration time, and may face late registration, make up tax, late filing, late payment of tax penalties. In order to help customers avoid unnecessary losses, Green Circle, as an official certified VAT service provider of Amazon Middle East, has rich experience in UAE tax agency and shares a real case to help sellers understand UAE VAT policy.

Green Circle was approached by a client who had registered his UAE tax code with his former agent but had not filed a return and was concerned enough to ask us what the risks were.

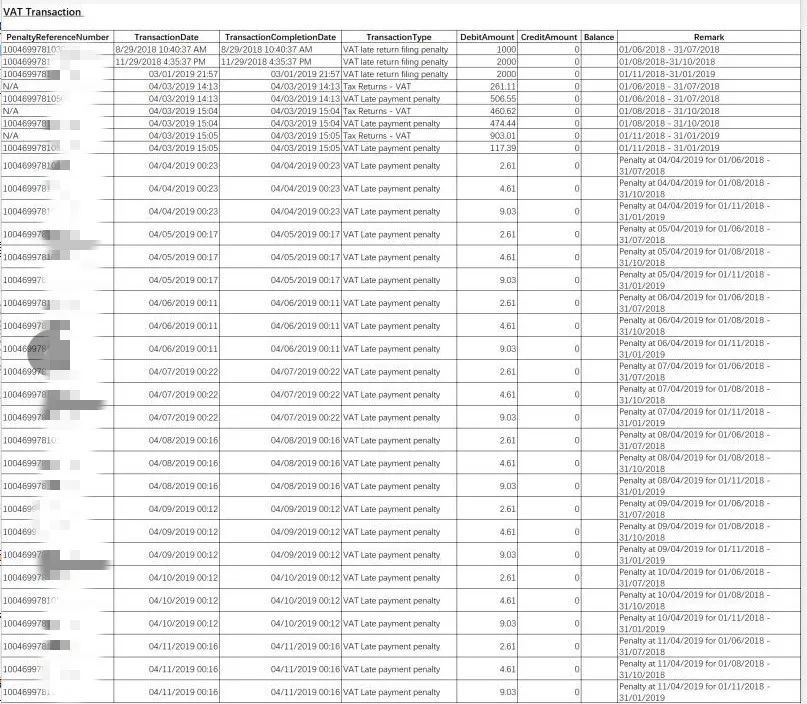

Case Client Penalty List

A quick look at the certificate shows us that his tax code was effective on June 1, 2018. According to the UAE filing period, the client has MISSED three filing periods: June-July 2018 (the first filing period required by the IRS), August-October 2018 and November 2018-January 2019.

We immediately breathed a sigh of relief for our client because the UAE tax authority is very strict and the penalties for late registration and filing are very high - in the event of late filing, penalties will be incurred the following day.

After the customer transferred the agent to Green Circle, we contacted the UAE Tax Department at the first opportunity to ask for a list of penalties that had not been received, and found that the penalties were higher than even the tax (7853.12 AED). For a new seller starting out soon, this is not a small amount of money, painstakingly operating accounts have not yet tasted the first bucket of gold, because of their own and the tax agent is unfamiliar with the tax policy, resulting in unnecessary distress and penalties.

Through the above real-life cases, I hope that when sellers choose a tax agent, they must screen the qualifications and service capabilities of the other party. At the same time, you should also understand the tax policy of your business market, so that you can operate with peace of mind and in compliance with the law.

The following is a complete list of all administrative VAT fines and penalties approved by the Federal Tax Administration (FTA) for the UAE. It is important for sellers to know that this list of penalties will apply to corporate or individual taxpayers who have violated the UAE's VAT laws.

01

Late Registration Penalty

Businesses or individuals making taxable supplies in the UAE above the minimum threshold for VAT registration should obtain VAT registration in the UAE and be issued with a Tax Registration Number (TRN). If the taxable person fails to register within the specified time period within 30 days of reaching the turnover limit, such VAT eligible businesses will have to pay a late fee.

Enterprises that fail to submit an application for registration within the stipulated time frame are subject to a fine of Dh20,000/-.

It is important to note that from January 1, 2018, B2C sales by overseas companies in the UAE fall under the mandatory registration area, removing the annual sales AED 187,500 limit.

02

Late Write-off Penalty

If the taxable person fails to notify the tax office of the cancellation within the time period specified by the tax authority for the mandatory cancellation, the mandatory cancellation time period is 20 working days from the date when the taxable supplies ceased to be supplied by the taxable person in the UAE. A taxpayer must apply for VAT write-off when it ceases to supply taxable goods or when its taxable turnover for the past 12 months is less than the VR threshold.

Merchants who fail to deregister within that time will be subject to a fine of Dh10,000.

03

Late filing penalties and penalties for late payment of tax

It is the duty of a VAT registered person to submit his/her VAT return within 28 days of the second month following the tax period. If the taxpayer fails to file the return on time, an initial AED 1,000/- will be charged as a penalty. If there is a subsequent delay in filing the VAT return or failure to file the VAT return, AED 2,000/- will be charged.

VAT registrants should also make payments to FTA by the due date for filing VAT returns. If the tax due is not paid by the due date, a 2% charge shall be levied on the unpaid VAT immediately after the due date. If the VAT remains unpaid after 7 days from the refund deadline, an additional 4% fee will be charged. In addition, if payment is still not made within one month, 1% will be charged for each day until the penalty reaches 300% of the unpaid tax.

Screenshot of original UAE tax law

04

Penalty for not being able to show the price including VAT

According to the UAE VAT law, when goods are sold at an indicated price, such indicated price must include tax. We can take the example of a hypermarket, supermarket or any retail store where the goods will be displayed on the shelves along with the price. According to the law, the displayed price should include VAT. Therefore, the displayed price will be the maximum price that the customer will have to pay when he receives the tax invoice.

If the taxable person fails to show the price including VAT, an administrative fine of Dh15,000 will be imposed.

05

Failure to provide compliant invoices

VAT is based on the concept of charging a tax on each level of consumption and will be structured in such a way that it will be a cost to the end customer. Therefore, it is important to provide proper documentation to the customers who pay VAT. Under the UAE VAT law, suppliers who are tax registered are obliged to issue a VAT invoice or credit note to their customers.

Under the UAE's VAT, if a taxable person fails to issue a tax invoice or refund note, they will be subject to a penalty of Dh5,000 per tax invoice or refund note.

06

Penalty for amending previous quarterly returns (Voluntary Disclosure Application Forms)

A VAT registrant can file a Voluntary Disclosure Form (VDF) 211 if there are omissions or any errors in the VAT return.There are fixed penalties and percentages for filing a VDF 211 depending on the time taken to file the VDF 211 to correct errors or omissions in the VAT return.

The potential fines for filing a voluntary disclosure form include:

Fixed Penalty: 3000 /-AED First Use VAT Disclosure Form

5000 /-AED for second use of VAT disclosure form.

Penalty based on percentage:

In the event that the tax authorities initiate an investigation and find that there are unpaid taxes, the penalty rate is 50% of the unpaid taxes.

30% if the taxpayer makes a voluntary disclosure after receiving notice of a tax audit but before the audit begins.

5% if the taxpayer makes a priority voluntary disclosure and notifies the tax audit.

07

Penalty for failure to keep financial records

Every VAT registrant is responsible for the correct and complete maintenance of corporate tax related files for a period of 5 years. They are also obliged to submit files or information when requested by the FTA or during tax audits.

If any taxable person carrying on business in the UAE fails to keep the requested records, or any such information will be subject to a fine of 10,000 AED/- for the first time and 50,000 AED/- if repeated.

08

Fines for unavailability of Arabic files

FTA allows records or files to be kept in Arabic or English. However, if requested by FTA, the business should produce the documents translated in Arabic. If any taxable officer fails to submit any record or information or any other supporting documents in Arabic as required by the authority, a fine of AED 20,000/- will be imposed.

Sellers who have read the whole article by heart, it is estimated that individuals are intimidated by the list of fines 😊 ~ in fact, do not panic, as long as the business is compliant, on time to file tax returns, the above are not a problem.