奧地利是歐盟最繁榮的國家之一,近年來網上銷售的增長速度明顯快於實體店銷售。作為Amazon歐洲站新星,奧地利強大的購買力受到了越來越多中國賣家的青睞。今天,綠圈圈小編先帶大家一起來瞭解學習奧地利增值稅基本知識,助力賣家們掘金新生地。

Distance selling

The current threshold in Austria is 35,000 Euro (since 1 January 2011).

遠程銷售閾值

奧地利從2011年1月1日起遠程銷售閾值是35000EUR。

Current legal basis

In general, if goods are dispatched or transported from an EU-Member State to Austria by a foreign supplier or on behalf of a foreign supplier to the below-mentioned customers, the supplies of goods are generally taxable where the goods are located at the time when dispatch or transport of the goods to the customer begins.

For distance selling however, there are special rules. Article 3 (3) – (7) Austrian VATAct 1994 stipulates that the place of supply of goods dispatched or transported by or on behalf of the supplier from an EU-Member State to another is the place where the goods are located at the time when dispatch or transport of the goods to the customer ends. Distance selling regime applies to certain types of recipients (especially private individuals as Amazon final consumers).

目前法律依據

一般來說,如果貨物是由歐盟境外的(非歐盟,例如我們中國企業)賣家在歐盟-成員國內有倉儲,向奧地利消費者銷售並從歐盟成員國倉庫發貨,則一般應在歐盟境內的貨物所在地(發貨國)徵稅。

然而,第3(3)-(7)條奧地利VATACT1994的遠距離銷售制度規定為由歐盟境外的賣家從位於歐盟-成員國(非奧地利的歐盟國家)倉儲向奧地利終端消費者銷售並發送商品,遠端銷售制度特別適用于作為亞馬遜B2C貿易的賣家。

Example例:

德國企業家或在德國有倉庫的中國企業家將貨物從德國轉移到奧地利的個人買家。一年銷售總額超過35000歐元的門檻,那麼從超過35000歐開始的銷售額,則在奧地利須繳納增值稅。德國企業家或中國企業家必須為在奧地利註冊增值稅號並在奧地利繳稅,發給這些奧地利個人的發票必須顯示奧地利的增值稅稅率!

注:根據1994年《奧地利增值稅法》第6條第1款第27項,沒有在奧地利建立業務或沒有永久位址的企業家沒有資格使用小企業計畫,(也即奧地利的小企業計畫不適合沒有奧地利倉儲的企業賣家。)

How to calculate the threshold

The delivery threshold must be calculated separately for each member country. When calculating the delivery threshold, only sales from distance selling regime should be taken into account.

Intra-community deliveries, charges for the delivery of new vehicles, charges for the delivery of excise goods and sales subject to differential taxation are excluded.

Entrepreneurs from other EU countries who deliver to private individuals in Austria must invoice with Austrian sales tax from the following time:

• 1. If the delivery threshold is exceeded in the previous year:billing with Austrian VAT from the 1st turnover of the current year.

• 2. If the delivery threshold is exceeded in the current year:Invoicing with Austrian VAT from the sales with which the delivery threshold was exceeded.

奧地利遠端銷售閾值如何計算

每個國家發往奧地利的銷售額分開計算,然後把非奧地利國家發奧地利的銷售加總,用這個加總值來計算遠端銷售額,看是不是超過奧地利閾值(35000歐元)。

庫存來自其他歐盟國家/地區的企業賣家符合如下其中一種情況,須開始註冊奧地利稅號並在奧地利繳納增值稅:

• 1.如果上一年超過遠程閾值35000歐元:從當年的第一筆營業額開始需在奧地利計算奧地利增值稅。

• 2.如果當年超過遠端銷售閾值,則從超過交貨閾值的銷售開始計算奧地利增值稅。

New EU regulation 2021

Please note that the threshold will be generally abolished beginning with 2021. That means from 2021 on distance sales will have to be taxed in each EU member state where the dispatch or transport ends.

2021年歐盟新法規

請注意,歐盟新法規從2021年開始取消該遠端銷售閾值。這意味著從2021年開始,遠端銷售將會在歐盟成員國按發貨國或目的國徵稅,而不會存在上述銷售閾值。

Application for a tax account number or a VAT number

Following documents are required for application.

· Verf 19: questionnaire for the assessment procedure

In addition: indication of sales channels (e.g.homepage, catalogue etc.)

Note:distance sellers are usually not allocated a VAT number since they only need a tax account number to account for the VAT due. However, if they need a VAT number, they have to fill in form ‘Verf 19’ giving sufficient reasons for their request.

· Verf 26: specimen signature sheet

· Valid VAT number or certificate of registration as taxable person (entrepreneur) issued by the Tax Office of the country the entrepreneur has established his business in (original)

· Copy of the company statutes

· Copy of the manager’s passport / ID

· Copy of the certificate of registration

申請奧地利增值稅號需要什麼註冊資料?

申請需要以下檔:

·(1)評估問卷(Verf19)

注意:遠端銷售商通常稅局不下發增值稅號, 但是,如果他們需要一個增值稅號,則必須填寫“ Verf 19”表格,以充分說明其要求。

·(2)申請簽名表(Verf 26)

·(3)公司在其國家/地區開展業務的國家/地區的稅務局簽發的有效的增值稅號或註冊證明(應納稅人)

·(4)公司章程的掃描件(備用)

·(5)法人護照/身份證影本

·(6)公司營業執照影本

Tax Representative

The appointment of a Fiscal Representative is only mandatory if the supplier has no permanent address, seat or fixed establishment in an EUMember State and if there is no appropriate mutual agreement procedure. The fiscal representative has to be an authorized recipient as well.

稅務代表

只有在賣家在歐盟成員國內沒有固定地址,所在地或固定機構並且沒有合法的雙方協定的情況下,才必須任命財務代表。財務代表也必須是授權作為稅局信件的收件人。

Disclosure/ Report of Incorrect or Incomplete Tax Declaration

If you have exceeded the Austrian distance selling threshold of EUR 35,000 Euro in previous years, but have not declared these supplies in Austria, you have to subsequently correct this and declare them in Austria. You can either report an incorrect or incomplete tax declaration to the tax authorities or fully disclose these supplies.

披露/報告不正確或不完整的納稅申報表

如果您在過去幾年中超過了奧地利遠距離銷售35,000歐元的門檻,但尚未在奧地利申報這些銷售,則必須隨後更正此狀況並在奧地利申報。您可以向稅務機關報告不正確或不完整的納稅申報單,也可以完全披露這些銷售狀態。

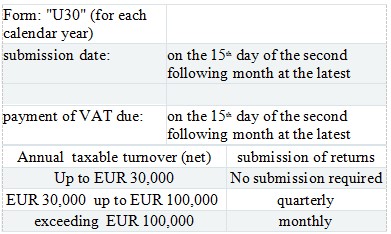

Submission of VAT Returns

In Austria there are VAT advance preliminary returns and VAT annual final returns.

· a. Preliminary VAT return

· b. Annual VAT return

提交增值稅申報表

在奧地利,增值稅申報須提交預付款初報和增值稅年報稅表。

–預付款初報(也即月報或者季報)

(1)截至申報日期是下個月的第二個月15日,(例如5月的銷售報告,須在7月15日之前提報)

(2)應繳增值稅:最遲在下個月的第二個月15日付款

▫年度應納稅營業額(淨額)申報表

1.如果一年稅前銷售額小於35,000歐元無需提交月報或者季報。

2.如果一年稅前銷售額大於35,000歐元小於100,000歐元,則可以季度申報。

3.如果一年稅前銷售額超過100,000歐元,則須月報。

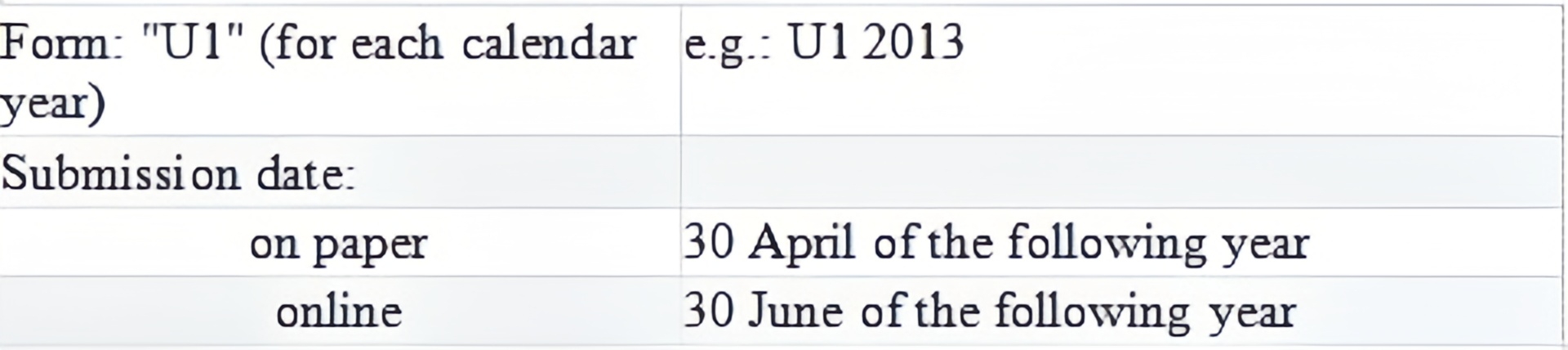

–增值稅年報稅表(也即年報)

可以通過線上或者紙質郵寄提交方式提交。網上提交的截至日期是下一年的6月30日,紙質郵寄提交的截至日期是下一年的4月30日。